ESG Investment Survey

ESG Investment Survey

ESG refers

to the use of environmental, social, and governance indicators to assess how

many businesses and countries have progressed in terms of sustainability. These

three metrics will be incorporated into the valuation phase when determining

which equities and bonds to purchase after enough information has been analyzed

on them.

ESG survey calculates the gap between the

discerned importance & actual practice

Although

the implementation of environmental, social, & governance (ESG) practices

in the transfer of risk, reinsurance, including insurance-linked securities

(ILS) sectors are viewed as quite significant. There is a clear difference

between perception and actual reality, according to a recent survey we

conducted with Synpulse.

We

collaborated with boutique consultancy company Synpulse to perform a study in

the third quarter of 2020 to assess the maturity of ESG in the insurance,

reinsurance, ILS, and risk transfer markets. It was the first of its kind

financial, social, and governance (ESG) survey, examining how risk transfer

organizations had integrated ESG considerations into their policies and

operations.

The

complete findings are being presented, and survey members will collect detailed

benchmarking details to assess their sophistication degrees in terms of

implementing ESG policies and activities compared to their competitors.

However, despite their importance, adoption

and ESG activities might not be as advanced as you would expect, with just a a small percentage of survey respondents taking behaviour that reflects their very

optimistic feelings about ESG. Various obstacles are seen as impeding ESG

acceptance in the insurance, reinsurance, ILS, and risk transfer sectors,

keeping back maturity and building this void.

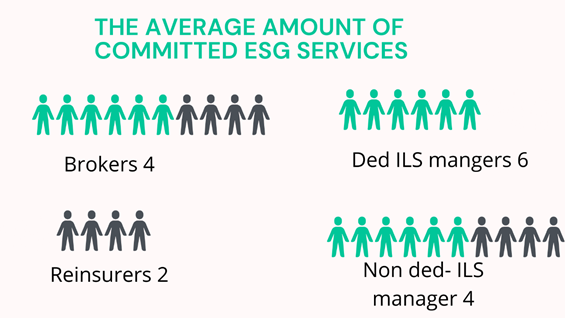

First, the

survey's findings indicate that several companies lack personnel devoted to ESG

adoption, with no committed individual and little commitment to date. Non-dedicated

ILS investment managers (i.e., more prominent asset managers who sell ILS

strategies), including insurers, are, unsurprisingly, better resourced than

devoted ILS fund managers.

Another

roadblock to implanting ESG activities at the organizational level is a lack of

well-identified, concrete targets in ESG strategies.

"Although

A large percentage of those surveyed accept that observable ESG targets are

being established, several of our people surveyed have expressed that they are

either not described precisely enough even in ESG strategies," Synpulse

clarified.

Participants

in our survey were also questioned whether they are calculating their ESG

footprints and there were evident disparities, with specific regions and

traditional investment market participants lagging. Participants

in our survey were also questioned whether they are calculating their ESG

footprints and there were evident disparities, with specific regions and

traditional investment market participants lagging.

"Most

committed ILS fund managers and reinsurers will be speeding up their activities

in this field by gradually including external players, which is a good

sign."

According

to Synpulse, 70 per cent of committed ILS hedge fund and underwriting

respondents said that calculating their ESG output with an external ranking or the score was critical for their company. In the financial risk value chain, the third challenge was accountability and disclosure. Although 90% of respondents

in our survey agreed that screening parties and components of risk inside the

production chain against ESG parameters are relevant, it's unclear whether this

is done in a meaningful way. Looking at reinsurance, retrocession, and ILS

contracts to see covered company underlying and analyze how each insured party

conducts business or accepts ESG presents considerable challenges. Although

ILS, like insurance and reinsurance, has relatively positive ESG

characteristics in providing catastrophe and more comprehensive insurance risk

resources and the social good it offers, things get a little murkier if you

look beneath the system itself. The farther down the risk transfer chain you

go, the less transparent things get, with retrocession Aires frequently getting

a good picture of the relevant insurance policies.

It will

create unique challenges for the ILS industry since confident institutional investors,

for example, need assurances that their contributions are not causing any

social or environmental damage. However, ensuring that the underlying insured

follows the same ethos is extremely difficult. As a result, a strict ESG review

of ILS contracts will undoubtedly reveal multiple gaps, emphasizing the value

of acceptance in the sector as end-investors become more concerned with

ensuring their allocations are ESG compliant in all asset groups. As the legislation takes effect, especially in Europe, accepting ESG can become

increasingly important for the ILS sector to maintain access to a diverse set

of investors.

There is still more work to be done, but the substantial perceived value of ESG signals that risk transfer, re/insurance,

and ILS market players would strive for greater acceptance and sophistication

of ESG considerations in their operations and decision-making.

Comments

Post a Comment